AB500

Dec 20

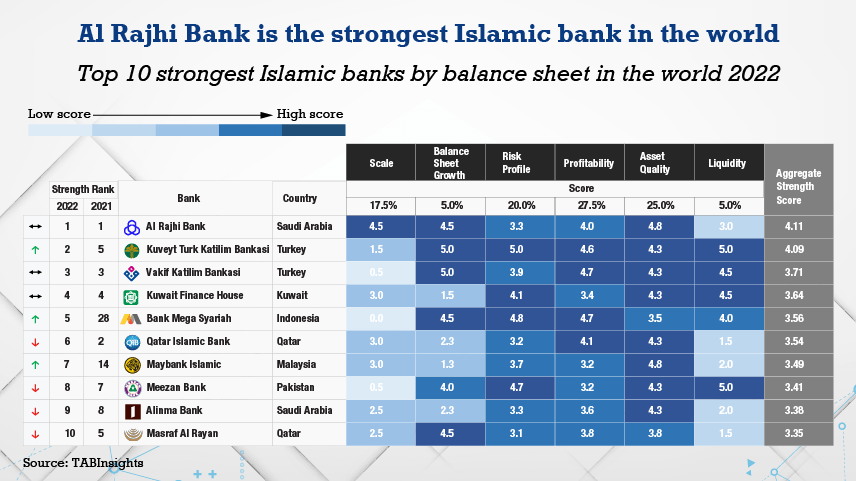

Al Rajhi Bank retained the top spot in the rankings of the largest and the strongest Islamic banks in the world. Malaysia had the most Islamic banks on the list, while Saudi Arabia held the largest share of total assets

.png)

.jpg)